It’s been a couple of eventful years of North American LNG production, with the industry at the center of a controversial Biden administration pause on permitting for non-FTA countries, and major global players like ADNOC and Woodside Energy moving into Gulf Coast LNG projects.

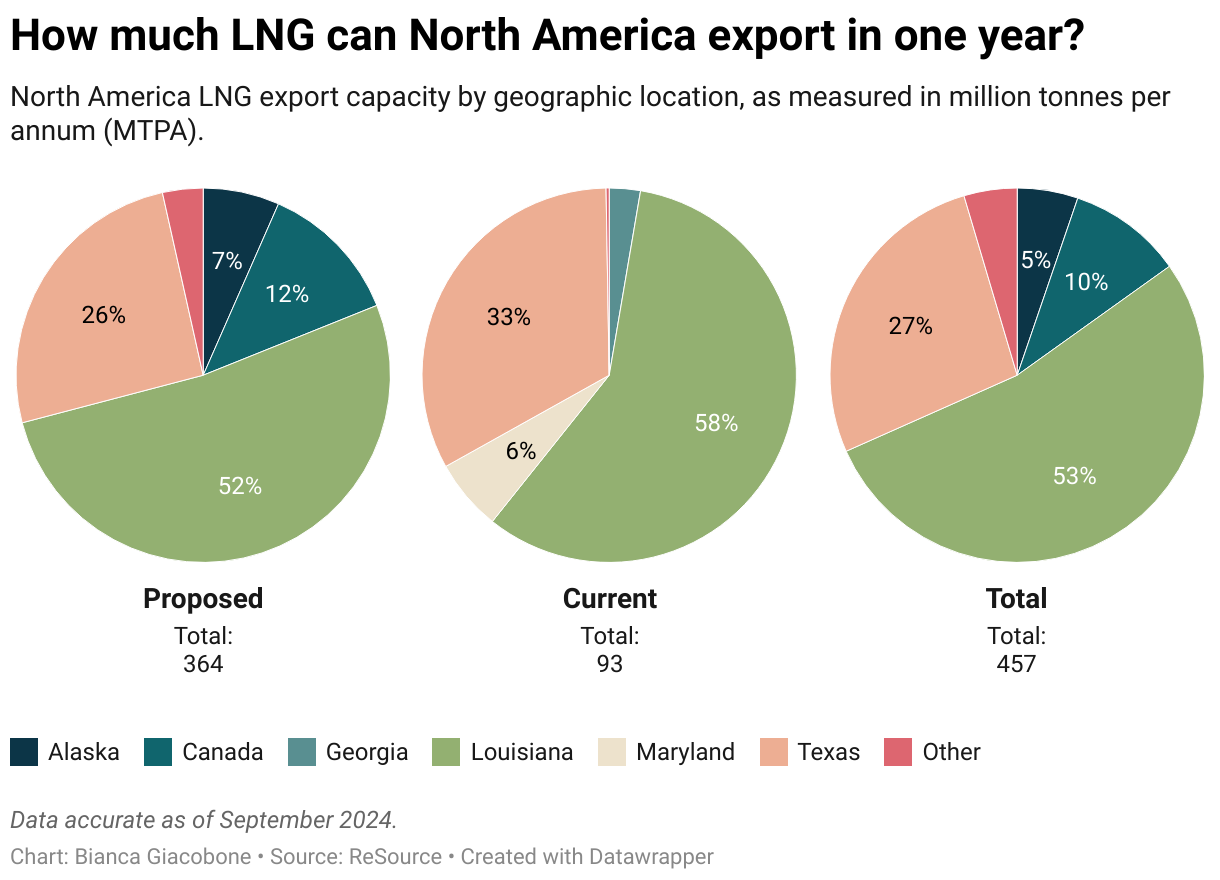

However, LNG investment and export opportunities in North America are still just getting started: there are 364 million tonnes per year of LNG export capacity in proposed North American LNG projects, compared to the 93 MTPA of LNG export capacity online now.

So far in 2024, the U.S. has shipped 56.9 million metric tons of LNG, according to global trade data analytics company Kpler, establishing itself as the biggest LNG exporter in the world for the second year in a row. As of August, Australia had shipped 54.3 million tons and Qatar 53.7 million.

Prices, however, have dropped around 25% on average in the first half of the year compared to 2023, according to the Energy Information Administration, as Europe, which has been desperately importing LNG ever since the beginning of the Russia-Ukraine war in early 2022, realigns itself towards renewable energy.

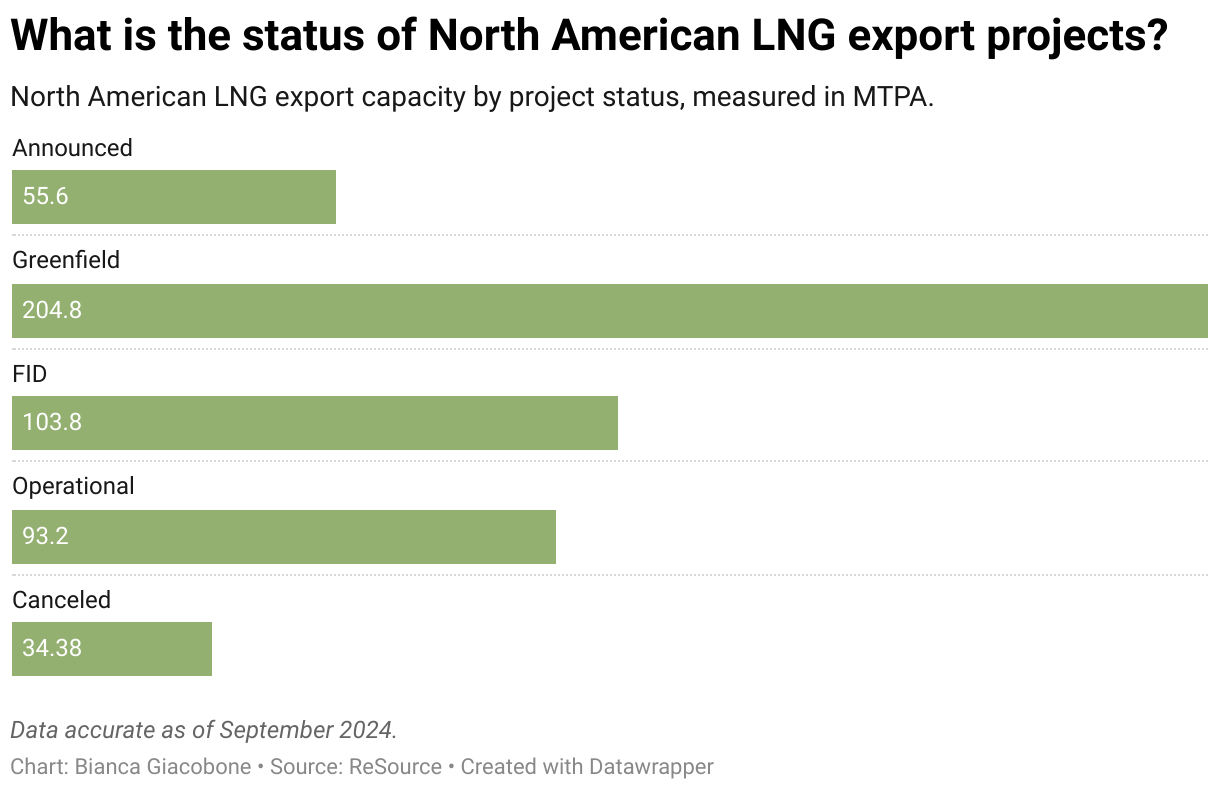

The slash in prices is only one of the challenges developers face while bringing large new export terminals online, alongside labor shortages, cost hikes, and legal disputes.

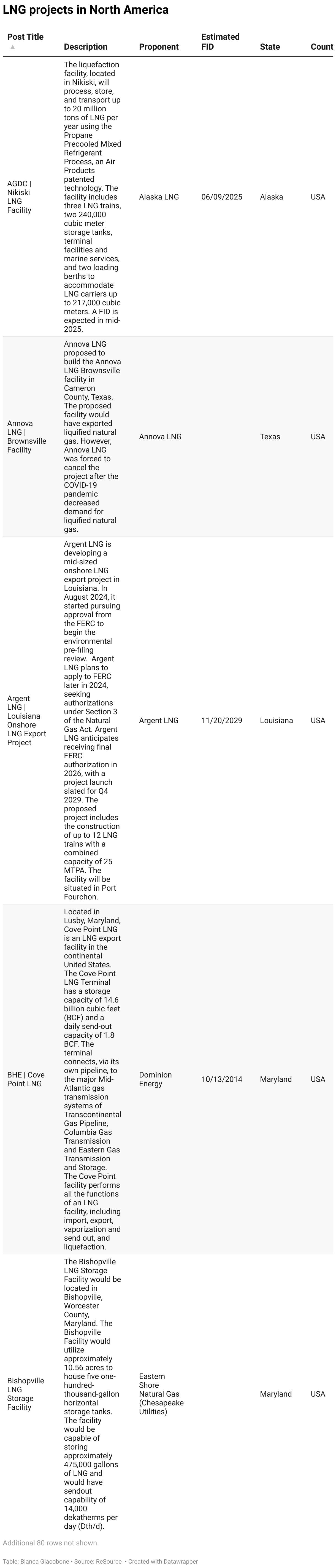

In August, for example, the U.S. District Court of Appeals for the D.C. Circuit vacated FERC’s certificate for two LNG projects in Brownsville, Texas, Glenfarne’s Texas LNG and NextDecade’s Rio Grande LNG, forcing the developers to apply for new permits, and threatening to delay FID.

The Rio Grande LNG project demonstrates another key feature of the LNG market: its capital intensity. The project last year reached a $18.4bn financing deal to fund construction of phase 1, making it the largest greenfield energy project in U.S. history.

Additional projects in the works are expected to bring online approximately 364 million tonnes per annum (MTPA) of LNG export capacity, with the vast majority of them concentrated in the United States. Over half of these upcoming projects are in Louisiana, 26% are located in Texas, and 12% and 7% are in Canada and Alaska respectively.

This would come in addition to the approximately 93 MTPA of LNG export capacity currently online in North America, 58% of which comes from Louisiana projects.

With over 73.8 MTPA of operational and upcoming capacity, Cheniere is the leading American exporter of LNG. Its Sabine Pass project in Louisiana, which first started exporting LNG in 2016, is the biggest operational facility in the U.S., if not the world, with an aggregate nominal production capacity of approximately 30 MTPA.

Cheniere is currently in the process of adding around 8 MTPA to the project.

Venture Global comes second, with four projects at various stages of completion and a total export capacity of around 57 MTPA.

As the amount of exported LNG grows, imports have been declining steadily, representing only around 1% of total natural gas imports into the U.S. in 2023.