As of April 2024, there are 42 blue ammonia projects in North America, including announced, greenfield, suspended, and projects that have reached a final investment decision (FID), according to data gathered by ReSource.

The vast majority of them, 34, are located in the United States. Over 60% of them are in the Gulf Coast region. Thanks to their attractive energy infrastructure and ports, from where producers could easily export the product to eager markets like Europe, Japan and South Korea, Texas and Louisiana are emerging as the undisputed North American hubs for blue ammonia.

Canada has eight blue ammonia projects, mostly concentrated in Alberta.

As a region with a strong oil and gas industry and already a natural ammonia hub sitting on major ammonia trade routes, North America, and the US in particular, is well positioned to dominate a future global blue ammonia market, according to a source familiar with the industry.

Overall, 20 North American projects are at a greenfield status, understood as comprising any project that has developed past a feasibility study stage, while an additional 19 have been announced, one has been suspended, and two have achieved the FID milestone.

OCI Global started building its blue ammonia project in Beaumont, Texas, in December 2022. The plant will receive the necessary low-carbon hydrogen supply from Linde, and, once it starts operations in 2025, it is expected to produce 1.1 million tonnes of blue ammonia per year, which, according to OCI, would make it the largest blue ammonia plant in the world.

One year later, in November 2023, Air Products received final investment approval for its $7bn clean energy complex in Louisiana, which will produce both blue hydrogen and blue ammonia.

Both companies have a robust network of existing relationships and infrastructure to rely on to offset the risks, which facilitates securing investments and offtake agreements, according to the source.

Another major blue ammonia project, Nutrien’s Geismar Clean Ammonia facility, which had a planned $2bn of capex, was officially suspended in August 2023 because of market uncertainty and high capital costs.

The project’s suspension could be a sign that some fertilizer producers are hesitant to invest in blue ammonia production if major energy players like ExxonMobil are also entering the space with their vast resources, according to another source familiar with the market. At the moment, around 70% of ammonia produced globally is used as a fertilizer, with the remainder used for industrial applications such as plastics, according to the International Energy Agency.

Since ammonia as an energy commodity is still a new idea with a yet-to-be-created market, there’s a general sense of uncertainty looming over the industry. Project developers are waiting for off-takers to move forward, while the off-takers are waiting for the project developers to take the first steps, especially as government subsidies like the 45V tax credit are still being worked out, according to the first source.

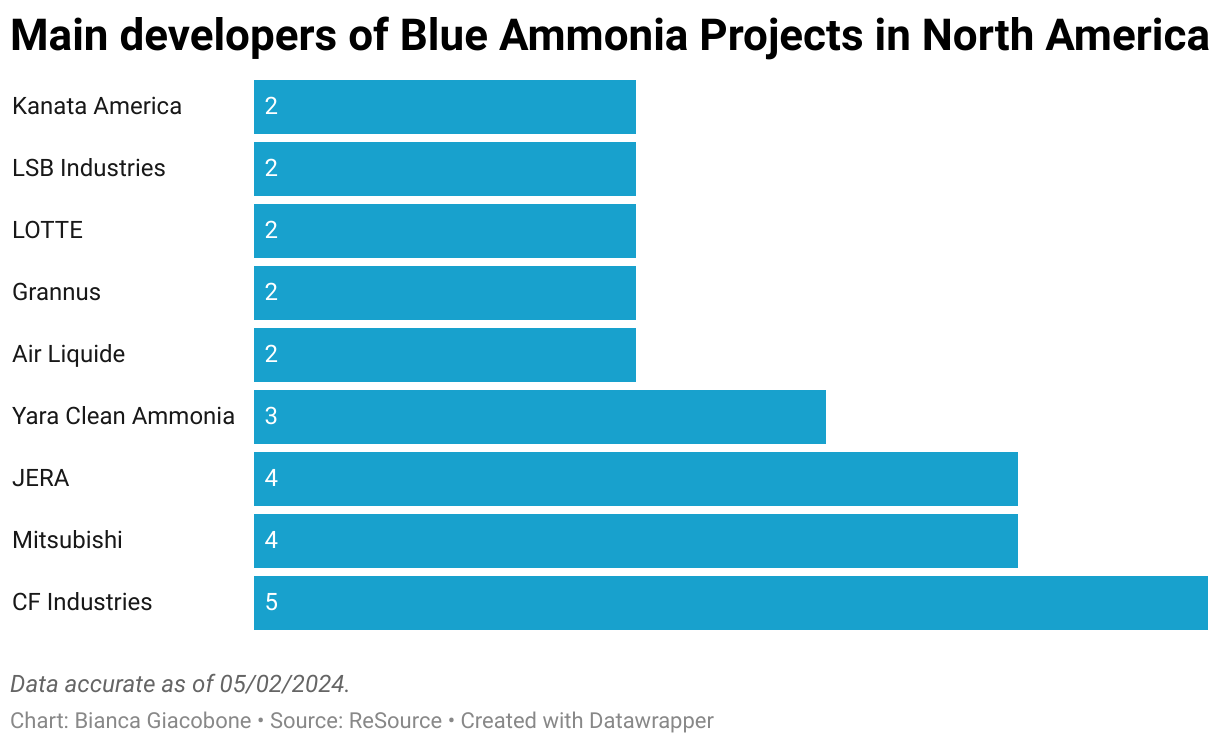

Of the nine main companies involved in blue ammonia projects in North America, however, the majority have been operating in the fertilizer industry for years.

With five ongoing projects, CF Industries is the most active one. As CEO Tony Will said in a recent investor call, the company expects the largest source of clean ammonia demand to come from Japan, and it has arrangements in place to develop one of its blue ammonia projects with both JERA Co. and Mitsui.

(ReSource initially recorded CF Industries’ arrangements with JERA Co. and Mitsui as two separate projects, but condensed them into one after executives said they would seek to align them under a single project during the investor call.)

The prediction is in line with Japan’s active role in the development of many North American clean fuels projects – around 4% of all clean fuels projects in North America have one or more Japanese firms involved as co-developers, equity investors, or off-takers. Accordingly, JERA and Mitsubishi come right after CF Industries for blue ammonia activity, being involved in four projects each.

Two things will play an important role in the future: what the carbon intensity reduction threshold is for a project to claim to produce blue ammonia, and how the nascent industry will adapt to the disarray in gas prices caused by Russia’s war in Ukraine.

The coming months will clarify which of the flurry of projects announced in the past couple of years are actually moving forward.